You’ve probably asked yourself this question before: Is insurance worth it? It’s not just about monthly premiums or confusing policy jargon. At its core, insurance is a financial tool designed to protect you from unexpected losses. But does the peace of mind it offers truly outweigh the cost? The answer isn’t black and white—it depends on your personal risk tolerance, financial situation, and life stage. In this article, we’ll break down the real value of insurance by analyzing the balance between risk and reward, helping you make an informed decision that fits your unique needs.

Insurance isn’t a one-size-fits-all solution. For some, it’s a lifeline after a car accident or medical emergency. For others, it feels like an unnecessary expense eating into their budget. The key is understanding what you’re really paying for: protection against financial ruin. Whether it’s health, auto, home, or life insurance, each type serves a distinct purpose in managing risk. And when you weigh that against potential rewards—like financial stability, asset protection, and long-term security—the value becomes clearer.

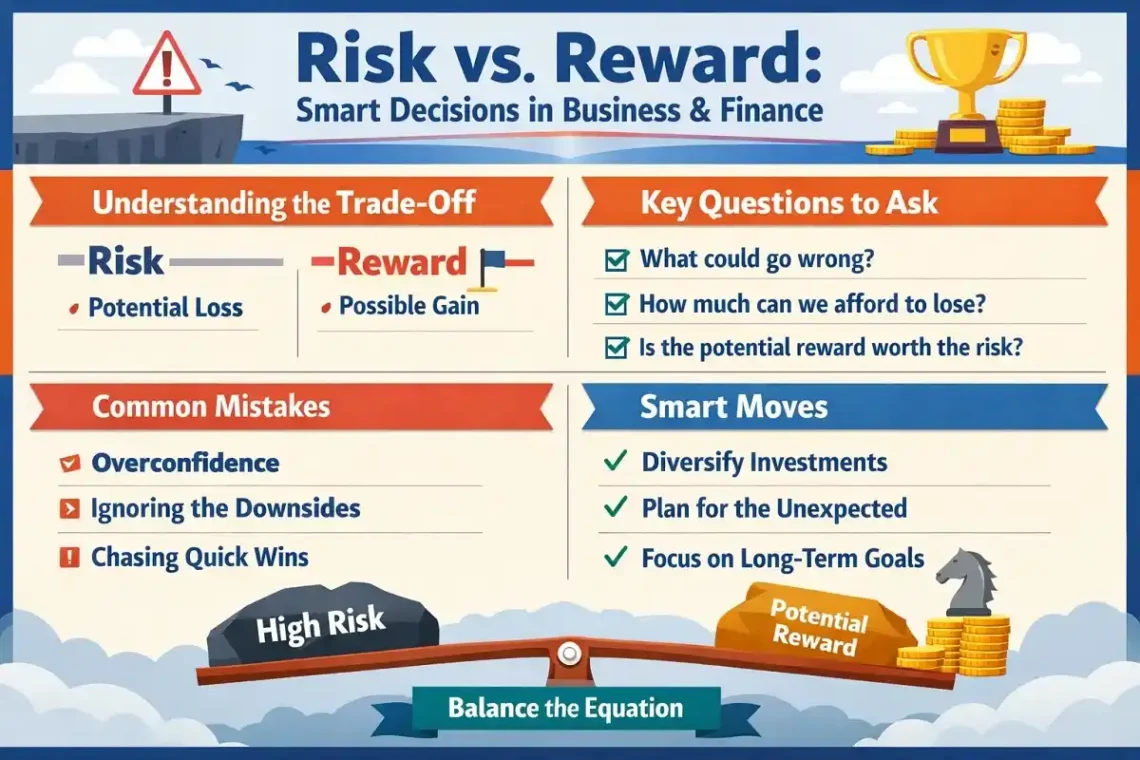

Understanding the Core Concept: Risk vs. Reward in Insurance

At its heart, insurance is a trade-off. You pay a regular premium to transfer the financial burden of potential losses to an insurer. In return, you gain protection against events that could otherwise devastate your finances. This is the essence of risk management. But not all risks are equal, and not all rewards justify the cost. That’s why evaluating the risk-reward ratio is essential before committing to any policy.

Let’s define the two sides of the equation:

- Risk: The possibility of a financial loss due to illness, accident, theft, natural disaster, or death. The higher the risk, the greater the need for coverage.

- Reward: The financial protection, peace of mind, and potential savings that come from having insurance when you need it most.

For example, a young adult with no dependents and a healthy lifestyle might question the need for life insurance. But if they own a home with a mortgage or have student loans co-signed by parents, the risk of leaving debt behind increases the reward of coverage. Similarly, someone living in a flood-prone area faces higher risk, making homeowners insurance not just wise—but essential.

How to Assess Your Personal Risk Profile

Not everyone faces the same risks. Your age, health, income, assets, and lifestyle all play a role in determining how much insurance you actually need. A 25-year-old renter in a low-crime urban area has different insurance needs than a 50-year-old homeowner with a family and a chronic health condition.

Start by asking yourself these questions:

- What would happen to my finances if I lost my income due to illness or injury?

- Could I afford to repair or replace my car, home, or belongings after a major loss?

- Do I have dependents who rely on my income?

- Am I exposed to natural disasters, high crime, or other environmental risks?

Your answers will help you identify which risks are most likely—and most costly—to you personally. This self-assessment is the foundation of smart insurance planning.

Types of Insurance: Where the Risk-Reward Balance Shifts

Different insurance products serve different purposes, and their value varies depending on your circumstances. Let’s examine the most common types and how the risk-reward equation plays out in each.

Health Insurance: High Risk, High Reward

Medical expenses are one of the leading causes of bankruptcy in many countries. A single hospital stay can cost tens of thousands of dollars. Health insurance acts as a financial safety net, covering everything from routine checkups to emergency surgeries.

For most people, especially those with chronic conditions or families, health insurance is not just worth it—it’s essential. The reward of accessing quality care without financial ruin far outweighs the monthly premium. Even healthy individuals benefit from preventive care and early detection of illnesses, which can save money and lives in the long run.

Auto Insurance: Mandatory Protection with Variable Value

In most places, auto insurance is legally required. But beyond compliance, it protects you from liability if you cause an accident, as well as damage to your own vehicle. The risk of a collision—even a minor one—can lead to costly repairs, medical bills, and legal fees.

The reward here is clear: financial protection and legal compliance. However, the value depends on your driving habits, vehicle type, and location. A new driver in a high-traffic city faces higher risk and thus greater reward from comprehensive coverage. Meanwhile, an older driver with a paid-off car in a rural area might opt for minimal coverage to reduce costs.

Homeowners and Renters Insurance: Protecting Your Largest Assets

Your home is likely your biggest financial investment. Homeowners insurance covers damage from fire, storms, theft, and more. Renters insurance, though often overlooked, protects personal belongings and provides liability coverage.

The risk of losing your home or possessions is low in frequency but extremely high in cost. The reward—peace of mind and financial recovery—makes this type of insurance highly valuable. Even renters benefit: replacing electronics, furniture, and clothing after a break-in can cost thousands, far more than annual premiums.

Life Insurance: A Reward for Loved Ones

Life insurance pays a benefit to your beneficiaries upon your death. It’s not about you—it’s about protecting those who depend on your income. The risk here is the financial hardship your family could face if you’re no longer there to support them.

The reward is stability for your loved ones: covering funeral costs, paying off debts, funding education, or replacing lost income. Term life insurance offers affordable coverage for a set period, making it ideal for young families. Whole life insurance includes a savings component but comes with higher premiums. The right choice depends on your goals and budget.

Disability and Long-Term Care Insurance: Overlooked but Critical

Many people underestimate the risk of becoming disabled or needing long-term care. Yet, a sudden injury or illness can leave you unable to work for months—or forever. Disability insurance replaces a portion of your income during such times.

Long-term care insurance covers costs associated with nursing homes, assisted living, or in-home care, which are not typically covered by health or Medicare. These policies are especially valuable for older adults or those with a family history of chronic illness. The reward is maintaining independence and protecting retirement savings.

When Insurance Might Not Be Worth It

While insurance is generally a smart financial move, there are situations where the cost may outweigh the benefit. It’s important to recognize these exceptions to avoid over-insuring or wasting money.

Low-Risk Scenarios

If you have significant savings, no dependents, and minimal assets, some types of insurance may offer limited value. For example, a single person with no debt and a robust emergency fund might not need life insurance. Similarly, someone with an older, fully depreciated car might skip comprehensive coverage.

The key is to assess whether the potential loss is something you could comfortably absorb on your own. If yes, the reward of insurance may not justify the ongoing cost.

Overlapping or Duplicate Coverage

Some policies overlap in coverage, leading to unnecessary expenses. For instance, your credit card might offer travel insurance, and your health plan might cover medical emergencies abroad. Paying for separate travel insurance on top could be redundant.

Review your existing policies to identify overlaps. Consolidating or eliminating duplicate coverage can save money without increasing risk.

High Deductibles and Low Claims Likelihood

Some insurance products come with high deductibles and low chances of claims. For example, pet insurance for a healthy young dog may cost more over time than the expected vet bills. Similarly, extended warranties on electronics often cost more than the average repair.

In these cases, the reward is minimal compared to the cumulative premium cost. It’s often smarter to self-insure by setting aside money in a dedicated savings account.

How to Maximize the Reward of Your Insurance

Even when insurance is worth it, you can take steps to ensure you’re getting the best value for your money. Smart shopping and policy management can significantly improve the risk-reward balance.

Shop Around and Compare Quotes

Insurance premiums can vary widely between providers for the same coverage. Use online comparison tools or work with an independent agent to get multiple quotes. Look beyond price—consider customer service, claims process, and financial stability of the insurer.

Bundle Policies for Discounts

Many insurers offer discounts when you bundle multiple policies—like auto and home—under one provider. This can reduce your overall premium while simplifying management.

Adjust Coverage as Life Changes

Your insurance needs evolve. Getting married, having children, buying a home, or retiring all impact your risk profile. Review your policies annually or after major life events to ensure coverage still aligns with your needs.

Raise Deductibles to Lower Premiums

If you have a healthy emergency fund, consider increasing your deductible. This lowers your premium and shifts more risk to yourself—but only if you can afford the out-of-pocket cost if a claim arises.

Take Advantage of Discounts

Many insurers offer discounts for safe driving, home security systems, non-smoking, or loyalty. Ask your provider about available savings opportunities.

Key Takeaways: Is Insurance Worth It?

So, is insurance worth it? For the majority of people, the answer is a resounding yes—when chosen wisely and tailored to individual needs. Insurance is not about eliminating risk entirely, but about managing it in a way that protects your financial future.

Here are the key takeaways:

- Insurance is a risk management tool: It transfers the financial burden of unexpected events to an insurer.

- The value depends on your personal risk profile: Age, health, income, and lifestyle determine how much coverage you need.

- Some insurance is essential: Health, auto, and homeowners insurance offer high rewards for most people.

- Others may be optional: Life, disability, and long-term care insurance depend on your dependents and long-term goals.

- Avoid over-insuring: Eliminate duplicate coverage and skip policies with low reward-to-cost ratios.

- Shop smart: Compare quotes, bundle policies, and adjust coverage as your life changes.

Ultimately, insurance is about peace of mind. It’s the quiet confidence that comes from knowing you’re prepared for the unexpected. While no one likes paying premiums, the real cost is what you stand to lose without protection.

FAQ: Common Questions About Insurance Value

Is it worth buying insurance if I’m young and healthy?

Yes, especially for health and disability insurance. Being young and healthy reduces your risk, but it doesn’t eliminate it. A sudden accident or illness can happen to anyone. Plus, premiums are typically lower when you’re younger, making it a smart time to lock in coverage.

Can I skip insurance if I have a lot of savings?

You might be able to self-insure for smaller risks, but major events—like a serious illness or lawsuit—can deplete even large savings quickly. Insurance protects your wealth from catastrophic losses that savings alone may not cover.

How do I know if I’m overpaying for insurance?

Compare your premiums to industry averages, review your coverage annually, and eliminate unnecessary add-ons. If your deductible is low and your claims are rare, you might be paying too much. Consider raising your deductible or switching to a more cost-effective plan.

Final Thoughts: Making Insurance Work for You

The question “Is insurance worth it?” doesn’t have a universal answer—but it does have a personal one. By understanding your risks, evaluating the rewards, and making informed choices, you can build a protection plan that truly serves your life.

Don’t let fear or confusion keep you from getting the coverage you need. At the same time, avoid the trap of over-insuring out of anxiety. The goal is balance: enough protection to sleep soundly at night, without draining your budget.

Insurance isn’t about predicting the future—it’s about preparing for it. And in a world full of uncertainties, that preparation is one of the most valuable investments you can make.